Politics, Pundits and Two Old Guys

Racing Towards November

Written By Philip Lockwood

As the 2020 presidential election campaign heats up I want to be clear that I endorse…….You will have to read to the end of the article to figure out where I cast my lot. Let’s take a break from the division and look at how markets have historically performed as a whole, then we will break down a few different investments that I am looking at, depending on the outcome of the election. The one thing that I know is that I am excited for 2021, even as the winner of the Oval Office will still be dealing with COVID-19, political and economic uncertainties, and civil unrest. I want to be very clear – what follows in this article is meant to show facts about past presidents and market performance. This is not an opinion piece and I will make every attempt to leave any bias out of this article.

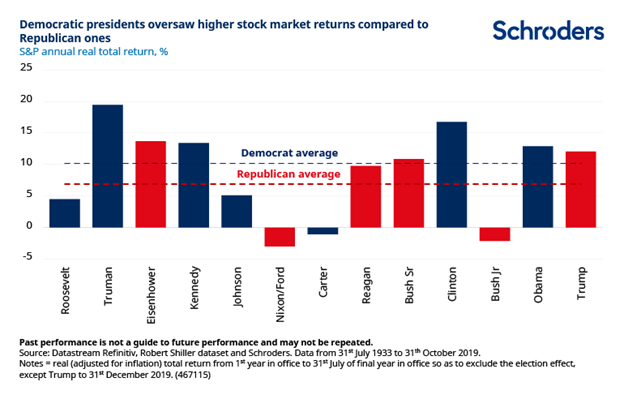

Let’s start out by looking at how markets have reacted historically when there has been a Republican or Democratic president. One of the misnomers I consistently hear is that the stock market performs better when the President is a Republican. This is simply not the case. The President does not have as big of an impact on the stock market as many people might think, and historically there have been very “stock market friendly” Republican Presidents, and very “stock market friendly” Democratic Presidents. You can see below- each individual Presidential term and the market performance.

The one thing to note here is that under the last 13 Presidents, only 3 times has the market been negative during that presidential period.

Please remember that each election year about 50% of the population thinks that if their candidate doesn’t win, the stock market is going to plummet. Today there is a narrative that if we have a Biden victory it could hit our pocketbook, but as you can see (above) we have only had one Democratic President with a negative stock market at the end of his time in office, and that was Jimmy Carter. One of the policy items that I am taking into consideration under a Biden presidency, that could have an effect on your portfolios, is the potential change to capital gains tax rates. When/If something like this were to take effect, we would pivot our strategy, as we are planning for a long term retirement. For years I have spoken with clients about having money in their taxable accounts, tax-deferred accounts and tax-free accounts (Roth IRA/Roth 401k) to position us to make changes when the tax code changes. This philosophy will not change as retirement will likely last 30+ years through multiple presidential cycles.

Of course, others are worried that a win for the incumbent could also spell trouble for U.S. equities. President Trump has proven to be even more unconventional than initially thought. For example, many businesses benefited from a significant corporate tax cut and reduced regulation, even as shifting views on trade and tariff skirmishes have made it difficult for companies to make long-term planning decisions.

By no means am I suggesting that a President Hillary Clinton would have proved better for equity markets, nor do we give much credence to today’s assertions that a President Biden would take a more aggressive COVID-19 stance and would somehow ensure more favorable medium-to-long term domestic growth at the expense of shorter-term prospects.

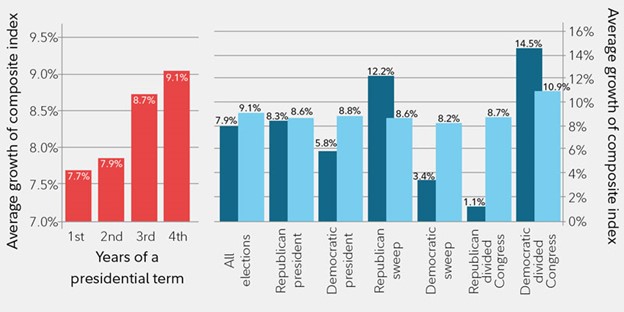

I would potentially suggest that we give too much credit (good or bad) to the President. In reality, the President normally has policies, but a large number of these policies take congressional approval. Let’s take a look at how the markets perform under multiple circumstances related to the President and Congressional parties.

As you can see, returns are very greatly based on which party the President is affiliated with and which party controls congress. The year of the presidential term would also appear to have a statistical impact on the rate of return during that period as you can see below.

*Dark blue bars in the right panel indicate returns during the first 2 years of a president’s term. The light blue bars show the 4-year return. Monthly data since 1789 (mix of S&P 500, Dow Jones Industrial Average, & Cowles Commission). Source: FMRCo

I give you all of this information and some pretty bar charts to say that, in the end, I don’t believe the President has a large impact on the market. I think it is more important to focus on the fundamentals. If you wait long enough, the long-term fundamentals of earnings and interest rates, labor growth and productivity, and the mean-reverting nature of an independent monetary policy, take over in driving long-term returns.

I believe that the economy and even, in a greater specification, the market, is bigger than the direction in which the political winds are blowing. I think there will be opportunities in specific equities no matter who is the President. This is where understanding policy can become important. Based on that thought, I have outlined some areas I think will do well, depending on who wins the election on November 3rd. (likely declared on a future date)

Which companies might be benefactors of each candidate’s policy –

Let me play Switzerland for a moment and mention companies that I think will benefit, no matter who wins the presidency. The number one area I would expect the next presidency to focus on with bipartisan support would be an infrastructure bill. Both parties are on the record acknowledging our crumbling infrastructure system and the needs for updated/safer roads, bridges, etc. The bipartisan support is why I have a high level of confidence that something like this could pass legislation and begin as early as 2021.

There are a few economic factors working in the favor of a large “rebuild America” type bill. Perhaps the largest argument to adding additional debt to our countries already ballooning debt issue, is that interest rates are incredibly low and aren’t seeing an increase any time in the near future. There is incentive for either party to pass an infrastructure bill while funding costs are cheap. Now is the time to borrow to spend on long neglected projects. Both candidates have highlighted the improvement of our infrastructure as a top priority. The second reason is our currently high unemployment level. Right now we have relatively high unemployment rates, and an infrastructure bill would go a long way in addressing this need in the labor force.

I can see two companies that would be benefactors of a new infrastructure bill and I will highlight each company below;

Caterpillar (CAT) –The earth moving company

I see this as a good play because, no matter who gets the contracts, they will likely be using Caterpillar machinery to deliver the finished products. Caterpillar is considered an economic bellwether as Its demand and sales reflect the heat of the economy. Caterpillar is the world’s largest construction-and mining equipment manufacturer. Over the past few years, Caterpillar has steadily cut back on capital expenditures, from almost 4.5 Billion in 2013 to just over 2.3 billion in 2017. They have also significantly increased their dividend from 42 cents quarterly in 2010, to $1.03 cents at present, good for a yield of 4.12%. From a valuation standpoint Caterpillar is currently trading at a forward P/E ratio of 23.2.

Vulcan Materials (VMC) – Not your favorite Star Trek character

Sticking with the Star Trek play, Vulcans are fictional, extraterrestrial, humanoid species, who attempt to live by logic and reason with as little interference from emotion as possible. This is the foundation for a solid portfolio manager. The company, on the other hand, is a play in the construction aggregates such as crushed stone, sand and gravel. Vulcan Materials is the largest U.S. producer of construction aggregates. It is also one of the top producers of construction materials, including asphalt and ready-mixed concrete.

The states in which Vulcan operates are poised to generate 72% of the total U.S. population growth this decade. Nineteen of the 25 fastest-growing markets in the U.S. are served by Vulcan’s operations. It makes sense that these areas will be a primary focus of federal infrastructure initiatives. Texas, California, Virginia, Tennessee, and Georgia contributed to 61% of Vulcan’s 2019 revenue. In 2019, Vulcan’s revenue grew 12% to $4.9 Billion, and net income surged 20% to $618 Million. It spent $239 million on operating and maintenance, $165 million on growth projects, and $167 million on dividends and share repurchases. Vulcan’s balance sheet presents a sturdy picture, while the cash flow has risen steadily in the past five years and debt is at a comfortable level. (https://www.fool.com/investing/2020/04/06/3-top-infrastructure-stocks-to-watch-in-april.aspx)

The two parties are as far apart on policy as they have ever been making the result consequential for markets. Each individual brings their own version of opportunity for investors. I will highlight a few areas of opportunity I believe each presidency can bring to the table. I will quote the famous value investor, Warren Buffett when he said, “Life is like a snowball. The important thing is finding wet snow and a really long hill.” I am using this blog post to identify what may be the wet snow that can quickly roll down a long (4 year) hill.

A Trump Presidency: Make America Great Again, Again (3 stocks for a Trump Presidency)

I will start out by addressing the scenario where President Trump wins his reelection campaign. As we sit here today, the President’s approval ratings have sagged, and both nation and swing state polls show that he meaningfully trails Joe Biden at this very early point in the race, but as we saw from polling in the 2016 election, it ain’t over until it’s over.

If history serves as a model, one area that will likely get a boost from a Republican presidency is military spending. We know that Trump likes the idea of a strong military. He has gone on record saying “I love the military”. He has even gone as far as creating a sixth military branch, Space Force.

Raytheon Technologies (RTX) – https://seekingalpha.com/article/4350458-raytheon-tails-you-win-heads-you-dont-lose

The underlying patriotism should serve companies like Raytheon Technologies well. Obviously, the coronavirus hasn’t dampened our adversaries’ enthusiasm to troll and test our military readiness. At a minimum I would think we would get a “flex” (increase in our military arsenal) from a President who won’t back down from a challenge. There is certainly a downside case to this stock involving their aerospace business and the lack of air travel. I believe Raytheon offers a downside-hedge in the bet on the recovery of air travel, thanks to the military side of its earnings and valuation. Defense contributed 54% of RTX’s sales in 2019. RTX currently trades at a forward PE ratio of 16.3 times. It is also paying a dividend of 3.12%

Lockheed Martin (LMT) –

Lockheed is the maker of Black Hawk helicopters, F-16 Fighting Falcon jets, F-35 Fighter and the Orion spacecraft. Lockheed didn’t perform particularly well during the Clinton years, but it enjoyed a nice run during George W. Bush administration, having two major wars certainly helped. The shares were mostly stagnated in the first half of Obama’s presidency, though they did enjoy a nice string of positive years during Obama’s second term. The company currently has a 144 Billion backlog of orders including a range of missiles and missile defense systems.

LMT shares remain reasonably priced at less than 15 times forward earnings, which is about in line with its average over the past year. The shares are also paying a respectable 2.8% dividend.

Writing about stocks that may benefit one party or another is awkward, but trying to discuss The GEO Group, especially in the present social climate takes the cake.

WARNING – Certain sectors of the stock market are probably best not discussed in polite company. The for profit private prison system isn’t a topic I am comfortable discussing at dinner parties…. wait what are dinner parties, do we even still have those? Anyway, you understand my point, but for your sake I will break down GEO in the event of a second Trump term.

The GEO Group (GEO)– One of the largest publicly traded prison landlords

GEO is technically a real-estate investment trust with a specialty in “evidence-based rehabilitation.” What this really means is that GEO stock is a platform for, shall we say, sophisticated private investors to exploit members of the at-risk communities.

Yes, they may be prisoners serving their time for their indiscretions against society. It’s just many people don’t feel comfortable monetizing this service. As you know, Trump bills himself as the “law and order” President. Thus, if he gets a second term, I would expect GEO stock could swing higher.

Biden Presidency – CHANGE version 2.0

I think a Biden presidency presents a few different opportunities that will be accompanied by a volatile stock market for a few main reasons. The first reason is CHANGE, I believe this was the phrase of the Obama administration and I believe it will be echoed by a Biden administration. One of the first things that Biden will attempt to implement and will likely be successful if we have a Democratic Congress is reversing a portion of the corporate tax rate cut that the Trump Administration enacted back in late 2017. The Biden campaign has floated the idea of increasing the corporate tax rate to 28%. I am not here to argue the merits of increased or decreased taxation, I am on the idea that reducing the federal deficit is a good idea, whether you can do this by increased taxation or by increased GDP as a result of lower taxation is an argument for another day.

This Biden corporate tax increase could reduce S&P 500 earnings by roughly $20 per share, driving investors out of different sectors of the U.S. stocks and hurting the dollar. A lower dollar isn’t necessarily a bad thing as it can increase exports, thus increasing GDP. If we do see a lower dollar I would look for the following areas as benefactors:

Emerging Markets –

The underperformance of emerging markets as a group isn’t exactly a mystery. Stale commodity prices and massive corruption scandals have effectively knocked Latin America out of the game for a better part of the last decade. Slowing growth in China and war in the Middle East certainly haven’t helped either. Biden’s administration would likely preside over a less confrontational trade agenda that should generally be better for emerging markets. In addition to the more favorable global trade agenda, the lower dollar will also help emerging markets with high debt to GDP ratios that are often reliant on dollar denominated debt and dollar funding may be seeing an even bigger tailwind. Some of the countries that may be seeing an easing debt burden from the weakening dollar according to debt to GDP ratios listed in the CIA World Fact book (https://www.cia.gov/library/publications/the-world-factbook/fields/227rank.html)

- Pakistan (67%)

- Brazil (84%)

- South Africa (53%)

- Sweden (41%)

- Argentina (58%)

The combination of a dovish Fed and a weaker dollar make Emerging Markets more attractive than they have been in years.

Gold –

Gold is an asset. As such, it has intrinsic value. As a rule, when the value of the dollar increases relative to other currencies around the world, the price of gold tends to fall in U.S. dollar terms. It is because gold becomes more expensive in other currencies. As the price of dollar moves lower, gold tends to appreciate as it becomes cheaper in other currencies. Gold can serve as a non-correlated asset to the stock market helping it balance the risk in some portfolios. I think gold can serve the right portfolio as an asset placeholder as we wait for stock indexes to sell at more reasonable valuations. A wise man once said, “to everything there is a season and a time for every purpose under heaven.”

Beyond the corporate tax increase Joe Biden wants to lay the groundwork to put the U.S. on track to achieve a “100% clean energy economy” by 2050 at the latest. To accomplish this, he plans to sign executive orders and push for Congress to pass legislation (which will be much easier if we have a democratically controlled congress) that established milestones for meeting key clean energy goals by 2025.

Brookfield Renewable Partners (BEP)–

Brookfield Renewable Partners should be a benefactor of such policy. Roughly three-quarters of the company’s funds from operations comes from its hydroelectric facilities. However, Brookfield also owns solar and wind power generation operations. Its pending acquisition of terraform will give it an even bigger presence in these arenas. BEP’s goal is to produce between 12% and 15% total returns annually. These returns do include the company’s attractive dividend, yielding around 3.26%.

While Biden is less focused on environmental issues than many of his Democratic peers, environmentalism and sustainability are a big part of his platform. From his campaign website: “From coastal towns to rural forms to urban centers, climate change poses an existential threat – not just to our environment, but to our health, our communities, our national security, and our economic well-being…Biden believes the Green New Deal is a crucial framework for meeting the climate challenges we face.”

Unsurprisingly, another major focus of a Biden administration would be healthcare. Biden was a champion for the Affordable Care Act and wants to protect and build upon the ACA, including giving Americans the option to buy a public health insurance plan similar to Medicare.

UnitedHealth Group (UNH) –

Such prospects could be music to the ears of UnitedHealth Group. The nation’s largest health insurer benefited tremendously when the ACA was first enacted. Nearly 28% of UnitedHealth’s revenue currently stems from its Medicare programs. They would also be a benefactor of Biden’s plan to lower prescription drug prices and promote the development of generic drugs, which would likely reduce the company’s expenses. UnitedHealth Group is currently trading at a forward P/E ratio of almost 18 and paying a dividend of 1.55%

What actions am I taking?

I think there are 3 things the next market movement will be dependent on:

- Getting Election results – this does not mean who specifically wins the election. It is having a clear uncontested winner within a reasonable time frame.

- Fiscal Stimulus – one thing I am confident about is that we will have additional fiscal stimulus from the congressional branch and the treasury. The size of the stimulus is likely to depend on who wins the presidential election and who holds the seats in congress

- Vaccine – When we get an effective vaccine then we can go back to living our “closer to normal” lives. This should boost many of the lagging sectors and provide some investment opportunity as things reopen and people are able to return to a more normal living situation.

In the short-term, I see plenty of volatility and that is a result of the three items above. One thing the broader market does not like is uncertainty. This is why I think a contested election could have a short-term negative impact on the market. If we do get a contested election, that will likely delay fiscal stimulus, which is desperately needed by small business owners, job seekers and individual households. We plan for the long term but don’t believe it would be prudent to turn a blind eye to the potential pitfalls in the next few weeks. If you have a discretionary Fidelity account that I manage, don’t be surprised to see additional cash positions as we are hedging against the negative potential of the items mentioned above and waiting for the market to present additional opportunity when the dust settles. If you are not a discretionary client then focus on the long-term plan. You can withstand some ups and downs as you focus on the next 15 to 20 years inside of your portfolio.

Now, lets get down to it….I endorse…

These are just a few ideas and the real work will begin after we have a Presidential decision. I believe we will likely encounter additional volatility on both sides of November 3rd, as we will likely not have a known outcome for several days, possibly weeks. As America chooses a direction for the next four years, please keep in mind that Washington is just one of numerous factors that drive stock market gyrations. I would never recommend a major alteration to a long-term asset allocation plan, based solely on politics.

It should come as no surprise that I endorse a portfolio designed individually for your risk tolerance and long-term goals, no matter who is in power in D.C. I want each of you to vote based on the policy that resonates with you and the candidate that echoes your ideals. I would not recommend you vote out of fear and I hope this expose gave you some reassurance that no matter who wins the election, I will do what I continue to do year in and year out: manage your money, your expectations, your financial plan and your financial sanity. If you know of anyone who is not receiving this type of council, please send them in my direction. I would be happy to sit down with them and have a conversation.

Philip Lockwood | Founder + Managing PartnerAddress: 3100 Ingersoll Ave Des Moines, IA 50312Phone: (515) 274-8006Email: Plockwood@parklandrep.comWebsite: Lockwood Financial StrategiesSecurities offered through Parkland Securities, LLC, member FINRA (FINRA.org) and SIPC (SIPC.org). Investment Advisory services offered through SPC, a Registered Investment Advisor. Lockwood Financial Strategies, LLC is independent of Parkland Securities, LLC and SPCSecurities offered through Parkland Securities, LLC, member FINRA/SIPC |